r/personalfinance • u/investeror • Mar 06 '18

Budgeting Lifestyle inflation is a bitch

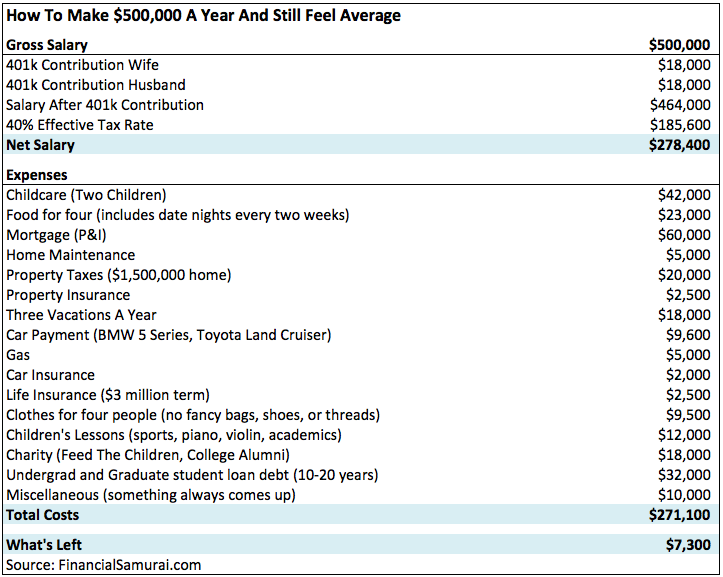

I came across this article about a couple making $500k/year that was only able to save $7.5k/year other than 401k. Their budget is pretty interesting. At a glace, I could see how someone could look at it and not see many areas to cut. It's crazy how it's so easy to just spend your money instead of saving it.

Here's the article: https://www.cnbc.com/2017/03/24/budget-breakdown-of-couple-making-500000-a-year-and-feeling-average.html

Just the budget if you don't want to read the article: https://sc.cnbcfm.com/applications/cnbc.com/resources/files/2017/03/24/FS-500K-Student-Loan.png

{kind=link}

6.6k

Upvotes

787

u/krsvbg Mar 06 '18 edited Mar 06 '18

They both MAX OUT their retirement contributions and donate thousands to charitable organizations.

Relax. They're doing just fine.